Fiona Hansen, Senior Managing Director at FTI Consulting, explores how COVID-19 has caused valuations to be brought back to basics, by having a look at the index value of shares as a percentage before and after the pandemic. To read more of Fiona’s insights into valuations, click here.

Fiona Hansen, Senior Managing Director at FTI Consulting, explores how COVID-19 has caused valuations to be brought back to basics, by having a look at the index value of shares as a percentage before and after the pandemic. To read more of Fiona’s insights into valuations, click here.

The Coronavirus (COVID-19) pandemic is having a much different impact on valuations than the global financial crisis (GFC). COVID-19 is essentially a health crisis that is adversely affecting the economy and business operations of many – but not all – companies. Most severely impacted are those companies with business operations linked to the human contact factors that contribute to the transmission of the virus, predominantly in travel, accommodation and hospitality. As such, one would expect these companies’ business operations to be negatively affected and hence their values to decrease.

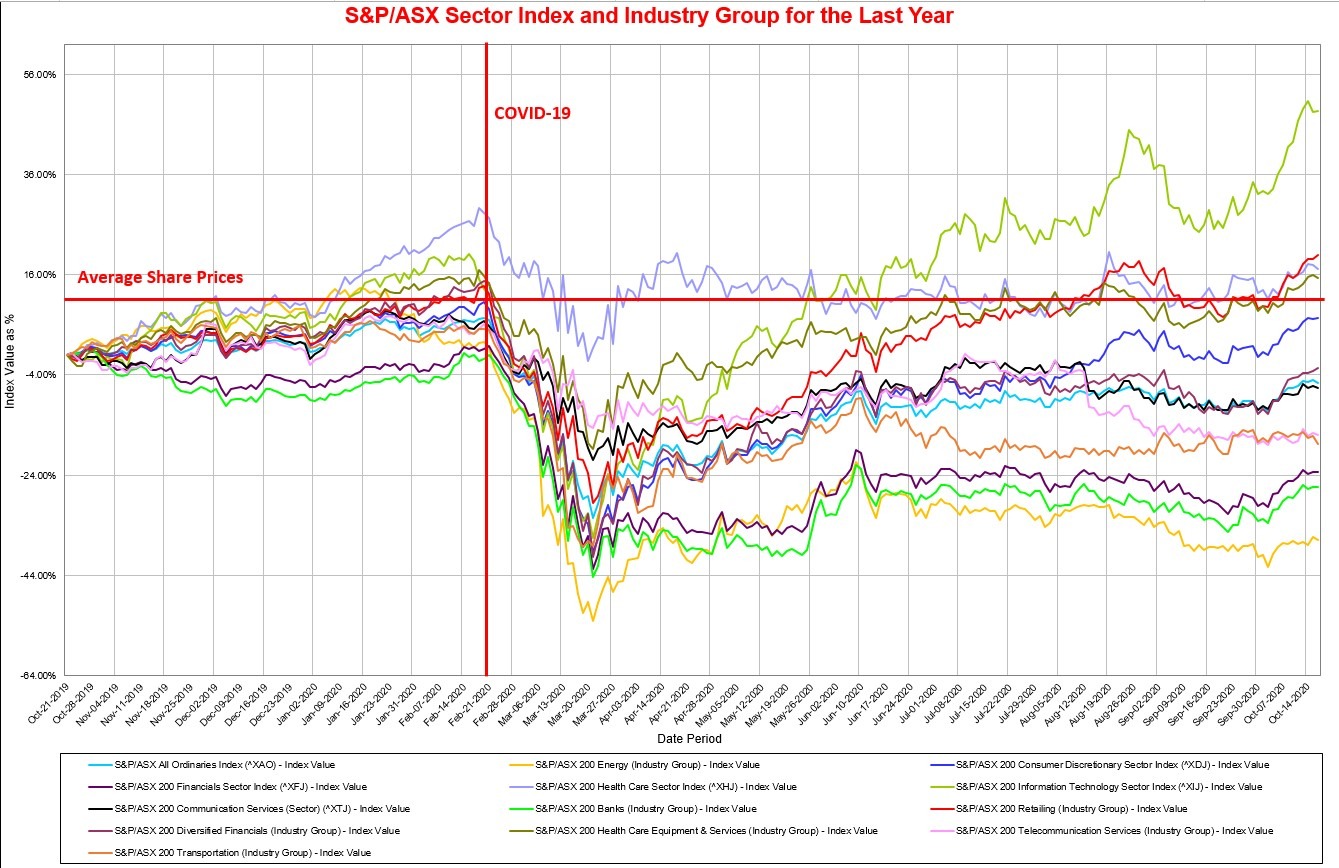

Notwithstanding the concentrated impact on particular sectors, financial markets exhibited panicked behaviour at the initial onset of COVID-19. Similar to other countries around the world, almost all listed company share prices in Australia decreased significantly at the onset of the crisis, regardless of whether their business operations were affected or not. Almost all companies’ share prices, as reflected by the sector indices, collapsed as shown by the major indices in the graph below. However, some companies’ share prices have already rebounded to levels at or above pre COVID-19.

Source: S&P Capital IQ (16 October 2020) Click on image to view full size

The companies included in the indices that did recover were IT companies, healthcare and retailing. This is largely because the goods and services of these companies have remained in high demand despite the population being restricted to their homes. For example, there was a surge in demand for IT-related services as people sought to remain connected; and a surge in demand for online health care services and equipment related to the needs brought on by the virus. Surprisingly, retail also rebounded well, although some retailers have had to quickly adapt their businesses to ‘online’ to meet increased customer demand.

Other sectors have not been able to respond to changes in customer demand and their share prices have not rebounded to pre COVID-19 levels. Examples of these sectors are energy, banks, financial institutions, transportation, and telecommunications.

The chart demonstrates that share prices have been volatile, primarily because of uncertainty perceived by investors, market sentiment, news stories and the market’s expectations for the economic outlook. However, share prices do not translate directly to a company’s underlying value. Despite share prices plunging over three months from late February, not all of these companies ‘lost’ value in line with share price declines.

Finding certainty in uncertain times

In contrast to share prices, an entity’s value is driven by its financial forecasts, expected profitability and perceived risk of achieving those forecasts. These are all, unsurprisingly, inputs to the discounted cash flow (DCF) method for valuing a company. Any valuation method using share prices as a valuation indicator, especially during COVID-19, would require careful scrutiny. Conceptually, a company should not lose its value because of market sentiment and investor reactions to uncertainty, especially when the company continues to make sales and maintain customer demand for its products and services.

The DCF method is traditionally the most technically sound valuation method. It uses forward looking forecasts and a corresponding discount rate that should also be forward looking. The current challenge for valuers is to find appropriate inputs to the discount rate. For a long time, valuers have been using traditional historical inputs such as market risk premiums and risk-free rates based on historical trends and dated research.

Until the markets begin to settle to a new ‘normal’, the DCF method should be the preferred valuation method. The DCF method is appropriate in changing and unpredictable market environments and can be equally appropriate in ‘normal’ economic conditions.

To understand the value of your business, whatever the circumstances, and for whatever reason – tax, financial reporting, transactions or disputes – contact one of our valuation experts. We provide bespoke and robust valuations that are fit for purpose and appropriately take into account the wider financial conditions, including the impacts COVID-19.

Fiona Hansen has over 25 years’ experience providing valuations through the dot com boom and bust, global financial crisis and now COVID-19. At FTI Consulting, our dedicated team of professional valuers is helping restore confidence to businesses and turbulent markets through the provision of well-evidenced and transparent independent valuations. For more information, contact one of our experts. Connect with Fiona via email or LinkedIn![]() .

.

The views expressed herein are those of the author(s) and not necessarily the views of FTI Consulting, Inc., its management, its subsidiaries, its affiliates, or its other professionals.

FTI Consulting, Inc., including its subsidiaries and affiliates, is a consulting firm and is not a certified public accounting firm or a law firm.

FTI Consulting is an independent global business advisory firm dedicated to helping organizations manage change, mitigate risk and resolve disputes: financial, legal, operational, political & regulatory, reputational and transactional. FTI Consulting professionals, located in all major business centers throughout the world, work closely with clients to anticipate, illuminate and overcome complex business challenges and opportunities. ©2020 FTI Consulting, Inc. All rights reserved. www.fticonsulting.com