HWL Ebsworth Tax Partners Shaun Cartoon and Nima Sedaghat and Special Counsel Renuka Somers discuss the ATO’s proposed stricter approach to demerger tax relief in a draft Taxation Determination.

Introduction

The ATO has released its much anticipated draft guidance on the demerger tax provisions in Taxation Determination TD 2019/D1 (the Draft Determination). To qualify for demerger relief, certain requirements must be satisfied under the “restructuring”. The broader the “restructuring” is defined, the less likely those requirements are to be satisfied.

In the Draft Determination, the Commissioner takes a very broad view as to what constitutes a “restructuring” for the purposes of the demerger provisions. The ATO’s view is that all the steps which occur under a single plan of reorganisation, even if legally independent of each other, contingent on different events, or may not all occur, will generally form part of the “restructuring”. This means that where the demerger happens in the context of a broader transaction, or series of transactions, it will be very difficult for the demerger to qualify for demerger relief.

- Background

Broadly, a demerger involves a restructuring of a corporate group by splitting it into two corporate groups. Both the group undertaking the demerger (the demerger group) and the group that is demerged (the demerged group) will be owned directly and in the same proportions by the existing shareholders of the “pre-demerger” group.

Shareholders commonly rely on two forms of tax relief provided under Australian tax law in respect of a qualifying demerger. Broadly, this relief takes the form of:

(a) Capital gains tax (CGT) relief: Owners of ownership interests in the head entity of a demerger group can obtain a roll-over to defer CGT consequences for the CGT events that happen to their interests under the demerger (Division 125 of the Income Tax Assessment Act 1997 Cth (ITAA 1997)); and

(b) Dividend relief: The dividend component of a demerger distribution is not treated as either assessable income or exempt income if the dividend is a “demerger dividend” and certain other requirements are satisfied (section 44 of the Income Tax Assessment Act 1936 Cth (ITAA 19360)).

Additionally, the demerger group is not subject to CGT on the disposal of the demerged group, as capital gains or capital losses made by the demerging entity are disregarded under Subdivision 125-C of the ITAA 1997.

For demerger relief to be available there must be a “demerger” as defined in section 125-70(1) of the ITAA 1997.

The first element of that definition is that there is a “restructuring” of a demerger group.

A number of additional requirements must also be satisfied for the demerger to qualify for tax relief. Two of the requirements that are often challenging, in practice, to apply are the:

(a) “Nothing else” condition: Broadly, under the restructuring, the holders of original interests in the head entity must receive new interests in the demerged entity and nothing else – hence, the demerger will generally not qualify if the shareholders in the head entity receive cash, shares (other than shares in the demerged entity) or other consideration under the demerger; and

(b) “Proportionality” requirement: Broadly, it must be the case that each owner of original interests in the head entity:

(i) acquires, under the demerger, the same proportion (or as nearly as practicable as the same proportion) of new interests in the demerged entity as each owner had in the head entity just before the demerger; and

(ii) has, just after the demerger, the same proportionate total market value of ownership interests in the head entity and demerged entity, as each owner had in the head entity just before the demerger.

The policy purpose behind the demerger relief provisions is to “facilitate the demerging of entities by ensuring that tax considerations are not an impediment to restructuring a business” and to “recognise that there should be no taxing event for a restructuring that leaves members in the same economic position as they were just before the restructuring” (paragraph 15.5 of the Explanatory Memorandum to Act No.90 of 2002).

In applying the above requirements, it is critical to define the relevant “restructuring”, particularly when viewed against the requirement that the owners of the head entity must acquire a new interest in the demerged entity “and nothing else” such as cash. Much therefore depends on how broadly (or narrowly) the “restructuring” is defined. If the “restructuring” is defined broadly (as the Draft Determination purports to do), then almost all corporate restructures that include a demerger as a component or step in a broader “restructure” will not qualify for demerger relief.

- The Draft Determination

The Draft Determination sets out what constitutes a “restructuring” of the demerger group. The ATO’s view is that:

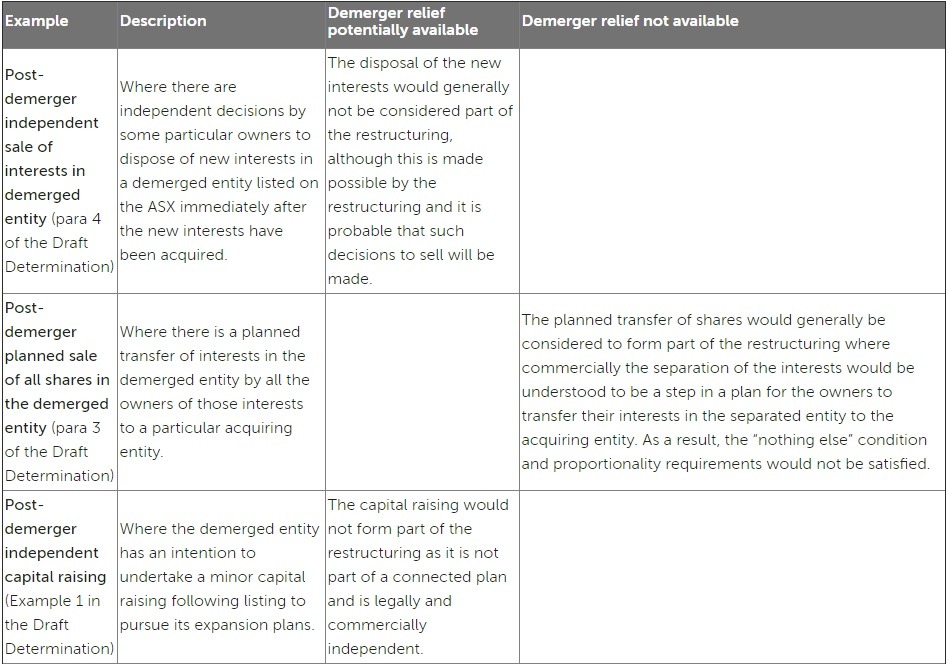

- What constitutes a “restructuring” is essentially a question of fact. All the steps which occur under a single plan of reorganisation will usually constitute the restructuring. It is not necessarily confined to the steps or transactions that deliver the ownership interests in an entity to the owners of the head entity of the demerger group, but may include previous or subsequent transactions in a sequence of transactions (paragraph 2 of the Draft Determination).

In this regard, a key factor in determining what transactions or steps form part of a single plan will be the proposal that is presented to the affected shareholders or unit holders. Reference would be had to the statements made by a company’s directors or the directors of a corporate trustee to affected shareholders or unit holders, pursuant to statutory and general law duties, as being representative of arguments made to persuade the affected shareholders or unit holders to support the necessary resolutions and other legal formalities that are required to implement the plan (see paragraph 66 of the Draft Determination).

- Transactions which are to occur under a plan for the reorganisation of the demerger group may constitute parts of the restructuring of the demerger group even though those transactions are legally independent of each other, contingent on different events, or may not all occur (paragraph 3 of the Draft Determination).

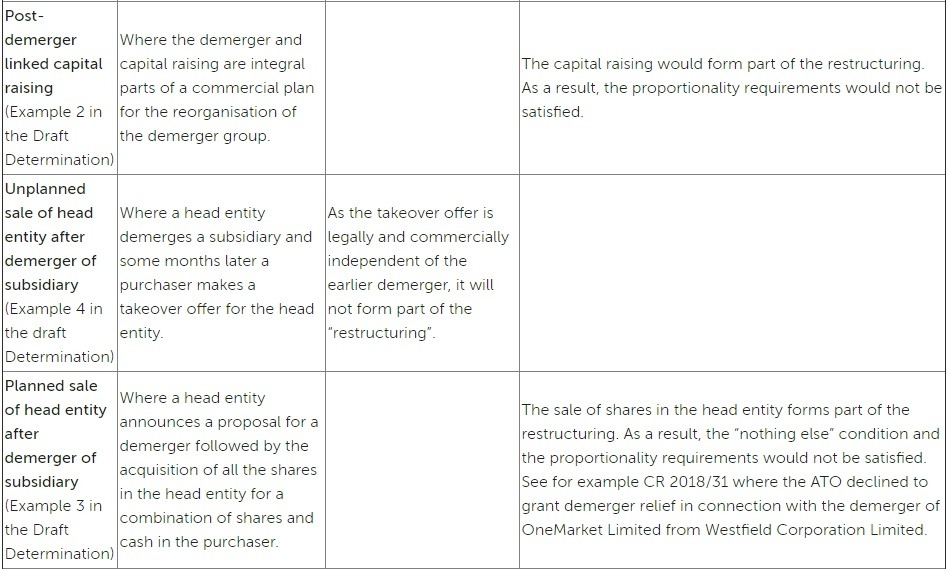

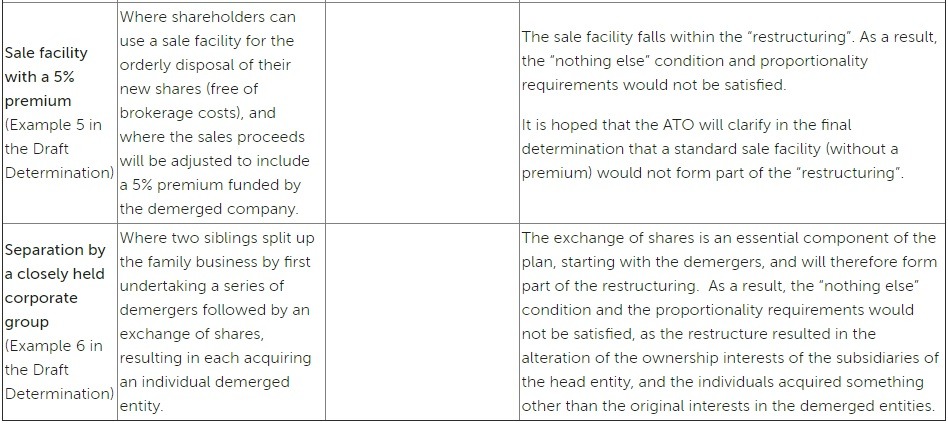

The ATO provides the following examples in the Draft Determination:

- Practical implications

If the Draft Determination is finalised in its current form, it is likely to have the following consequences:

- All but the most “vanilla” of demerger transactions will raise serious risks that demerger tax relief will not apply. In practice, more companies will now seek comfort from the ATO, in the form of a ruling, that demerger relief is available. For example, where a standard sale facility is used (without payment of a premium);

- In a global M&A context, where the decision to proceed with a significant corporate transaction is not solely determined by Australian tax considerations and where the Australian investor base is potentially small (eg. employee shareholders), we would expect to see “non-qualifying” demerger transactions still proceed, notwithstanding that Australian shareholders will be unable to access demerger tax relief;

- Company Boards will engage in longer term strategic business planning that might result in demergers of non-core business assets well before a potential suitor for the acquisition of either the core or non-core business is found. Ironically, this could increase the number of demergers that we see in the market. Significant care should be taken when preparing internal Board and external shareholder communications describing the stated purpose and objective of corporate transactions, as these communications are likely to be taken by the Commissioner as being representative of the restructure proposal for the purposes of determining whether the transactions or steps formed part of the single plan of the reorganisation;

- In an employee share scheme context, companies must always be careful not to provide share plan participants with “something else” in connection with the demerger. For example, if a company agrees with those employees who move across to the demerged entity that it will procure the demerged entity to grant replacement awards to the employees after the demerger, such employees will acquire contractual rights against the company. The issue here is whether such contractual rights would constitute “something else” in connection with the demerger. As long as the arrangement that leads to the acquisition of the contractual rights is provided for in the plan rules, then it should be able to be argued that the contractual rights are acquired by the employees under the relevant plan rules and not under the “restructuring”. However, the breadth of the ATO’s views as to what constitutes a “restructuring” in the Draft Determination may now cast some doubt on this analysis, especially if the plan rules are amended contemporaneously with the restructure; and

- As alternatives to non-qualifying demergers, companies might consider:

- an “old style” (pre 1 July 2002) demerger – for example, in circumstances where the demerger distribution can appropriately be debited to the share capital account and where the shareholders will suffer a reduction to their cost base as a result of a CGT event G1 (and potentially a capital gain); or

- a trade sale of the businesses or subsidiaries followed by a return of capital in appropriate circumstances.However, such approaches essentially limit potential demergers to entities with no significant disparity between the market value of the businesses being demerged and the cost base of those assets; as was the case with the demerger of entities within the Amcor, Boral and BHP groups in the early 2000s. Further, they have the potential to trigger the anti-avoidance rules in section 45B of the ITAA 1936, if the share capital reduction is construed as a scheme pursuant to which a taxpayer is provided with a capital benefit for a purpose of obtaining a tax benefit, with the consequence that the tax benefit is ultimately treated as a dividend taxed at higher rates (section 45C of the ITAA 1936).

Disclaimer: The material contained in this publication is of a general nature only and is based on the law as of the date of publication. It is not, nor is intended to be legal advice. If you wish to take any action based on the content of this publication we recommend that you seek professional advice. Please contact the authors if you have any queries about this Draft Determination or if you would like assistance in providing comments to the ATO.

Shaun Cartoon is a Partner with the Taxation team based in Melbourne. Shaun practices in corporate, international and employment taxes, with particular expertise in M&A and corporate transactions, employment taxes (including employee share schemes) and superannuation. Shaun also has significant experience in complex tax audits and disputes and has litigated significant tax cases through the Australian courts. Shaun is ranked in the Legal 500 Asia-Pacific as a Band 1 Next Generation Lawyer in Tax and was recognised as a ‘star’ advisor in employee share schemes by the Global Equity Organization. Shaun’s clients describe him as being “accessible” and having “a strong command of technical detail and the ability to apply this to complex situations in a pragmatic and commercial manner”. Shaun is Vice Chairman of the Tax Institute’s Breakfast Club Committee and also sits on the Tax Institute’s Superannuation and Employment Taxes technical committees. Prior to joining HWL Ebsworth, Shaun practised at top tier and magic circle law firms. Contact Shaun at scartoon@hwle.com.au or connect via LinkedIn ![]() .

.

Nima Sedaghat is not a typical tax lawyer. He is passionate about providing practical solutions to complex taxation issues, energetic in his approach and proactively identifies opportunities for his clients. Nima specialises in transaction taxes and regularly provides transaction and structuring assistance to Australian and foreign entities in the financial services, funds management and M&A sectors. In addition to being a lawyer, Nima is also a qualified Chartered Accountant. Contact Nima at nsedaghat@hwle.com.au or connect via LinkedIn

Nima Sedaghat is not a typical tax lawyer. He is passionate about providing practical solutions to complex taxation issues, energetic in his approach and proactively identifies opportunities for his clients. Nima specialises in transaction taxes and regularly provides transaction and structuring assistance to Australian and foreign entities in the financial services, funds management and M&A sectors. In addition to being a lawyer, Nima is also a qualified Chartered Accountant. Contact Nima at nsedaghat@hwle.com.au or connect via LinkedIn ![]() .

.

Special Counsel Renuka Somers assists private clients, corporate groups, and their advisers resolve complex tax issues, restructure business groups and succession planning. Renuka specialises in federal tax, trusts, tax consolidation, and Family Office matters. She has published numerous articles on tax and trusts issues in the Taxation in Australia journal and has also presented on these topis for The Tax Institute of Australia. Contact Renuka at rsomers@hwle.com.au or connect via LinkedIn

Special Counsel Renuka Somers assists private clients, corporate groups, and their advisers resolve complex tax issues, restructure business groups and succession planning. Renuka specialises in federal tax, trusts, tax consolidation, and Family Office matters. She has published numerous articles on tax and trusts issues in the Taxation in Australia journal and has also presented on these topis for The Tax Institute of Australia. Contact Renuka at rsomers@hwle.com.au or connect via LinkedIn ![]() .

.

You can also connect with HWL Ebsworth via LinkedIn ![]() and Twitter

and Twitter ![]()