Michelle Maynard, Partner at Carbon Accountants and Business Consultants, discusses how Fringe Benefits Tax might apply to your firm’s end-of-year Christmas party. There are some instances where these non-cash benefits will not be subject to FBT, she writes.

|

With 2018 drawing to a close, (how is it October already!?) our thoughts turn to the end of year Christmas Party. While it is a fantastic opportunity for employers to celebrate the end of year, employers should be aware of the tax consequences of hosting Christmas parties for their staff.

When employers provide certain non-cash benefits are benefits to their employees and associates (including past, future and current employees and their spouses and children, these are called fringe benefits. Fringe benefits are subject to fringe benefits tax (FBT) – at a rate of 47% on the grossed- up taxable value of the benefit given.

There are some instances where these non-cash benefits will not subject to FBT. While Christmas Parties are not specifically dealt with in FBT legislation, the following types of FBT exempt benefits should be taken into consideration when determining if FBT applies to your end of year Christmas party.

1. Exempt property benefits – The costs (such as food and drink) associated with Christmas parties are exempt from FBT if they are provided on a working day on your business premises and consumed by current employees. The property benefit exemption is only available for employees, not associates.

2. Exempt minor benefits – If the party does not satisfy the exempt property benefits (i.e. it is held off site or no held on a working day) it may still be an exempt minor benefit. In order to be an ‘exempt minor benefit’, the cost per employee, and associate, must be less than $300.

If the employer also provides gifts at the Christmas Party, the provision of the gifts may separately qualify as an ‘exempt minor benefit’, as long as the value of the gift is also less than $300. This is because for the purposes of the exempt minor benefits exemption, the value of each benefit provided (e.g the Christmas Party and the gift) can separately qualify as an ‘exempt minor benefit’ if the value of each separate benefit falls below the $300 threshold.

The minor benefits exemption is not available for meal entertainment fringe benefits (e.g. food and drink at the Christmas party) if the employer uses the 50:50 split method when preparing the annual FBT return. This is where the employer elects for 50% of the GST-inclusive cost of total meal entertainment to be subject to FBT and the other 50% to be exempt. For the minor benefit exemption to apply, the actual method to value meal entertainment expenses must be used.

The amount of FBT payable on the Christmas Party depends on:

-

- When the party will be held

- Where the party will be held

- For whom the party will be held

Generally, when an employer provides taxable fringe benefits to employees or their associates, an employer may be able to claim GST credits and income tax deductions in respect of these expenses. However, no GST credits or tax deductions may be claimed when providing FBT exempt benefits.

The ATO provides some more information regarding how FBT applies in different scenarios:

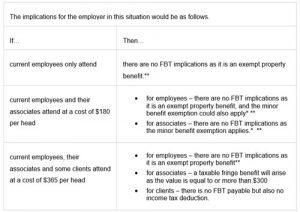

A small manufacturing company decides to have a party on its business premises on a working day before Christmas. The company provides food, beer and wine.

* Where the benefits are indicated as qualifying for the minor benefits exemption, it is on the basis that the necessary conditions have been satisfied.

** No GST claimable and not income tax deductible.

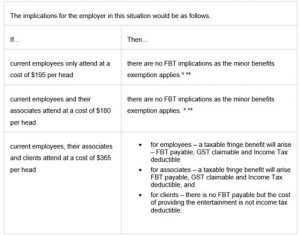

But how does this change if the event was held at a nearby restaurant?

** No GST claimable and not income tax deductible.

Top tips to avoid FBT on your Christmas Party?

1. Keep the cost under $300 per person

2. Choose your location wisely – if you can host the event onsite – great! If you prefer to go offsite, ensure you satisfy point number 1!

3. Keep the party to employees only – if associates of employees attend the party, even if it is held on work premises during working hours, FBT will apply. If you want to invite associates of employees, again, ensure you satisfy point number 1!

And remember, when the silly season is over, the same FBT rules apply to work functions and celebrations such as Melbourne Cup, employee birthdays, farewells or business milestones, but this list is by no means exhaustive.

Michelle partnered with Carbon in 2017, bringing a wealth of experience in accounting and bookkeeping. Her extended suite of services covers everything from tax accounting, planning and estimates, to cloud integration, payroll and SMSF. Michelle started her career as a cadet in the Australian Taxation Office, then as a graduate at PwC. Before joining Carbon, she was a manager at PKF, bringing a wealth of knowledge and experience to the team at Carbon. Michelle specialises in providing tax and accounting advice to SMEs and HNWIs and their family groups, working to achieve the most effective strategies for them, both financially, tax effectively, and to help achieve their desired lifestyle.

Contact Michelle at Michelle.m@carbongroup.com.au You can also connect with Carbon Accountants and Business Consultants via Facebook, Twitter and LinkedIn