D ung Lam, Special Counsel at Coleman Greig Lawyers, shares valuable tips to address the issues raised when your SMSF has breached superannuation law, by getting on the front foot and engaging early with the ATO. She discusses how the ATO considers the administrative penalty regime and how they approach penalty remission.

ung Lam, Special Counsel at Coleman Greig Lawyers, shares valuable tips to address the issues raised when your SMSF has breached superannuation law, by getting on the front foot and engaging early with the ATO. She discusses how the ATO considers the administrative penalty regime and how they approach penalty remission.

On 15 October 2020 the ATO issued Practice Statement PS LA 2020/3 (Practice Statement) which outlines:

- how the ATO considers the administrative penalties regime applies to superannuation law breaches made by self managed superannuation funds (SMSFs); and

- what considerations the ATO takes into account when considering remission of such penalties.

This update focuses on salient points raised by the Practice Statement.

The Practice Statement is a ‘mixed bag’ with some good aspects and some less kinder aspects. On the plus side the Practice Statement acknowledges the harshness of the administrative penalty regime where multiple penalties can apply to what practically is one breach and expressly provides for remissions where the result is unintended or unjust. The Practice Statement’s outline of factors which the ATO sees as relevant for penalty remission is also welcome since the statutory provisions on penalty remission in section 298-20 of Schedule 1 to the Taxation Administration Act 1953 (TAA) are silent on the matter. On the other hand the issue of the Practice Statement signals an intent by the ATO to take a much firmer stance on penalty remissions than it has in the past where it was felt that too many penalties were being remitted for behavior which should have been punished.

What the Practice Statement mostly reinforces is the imperative need for SMSF trustees who discover a superannuation breach to seek specialist superannuation advice promptly and if necessary to access the ATO’s early engagement and voluntary disclosure service as soon as possible. Penalty remission will be a much harder process if the breach is picked up by the ATO.

How the ATO considers the administrative penalty regime operates

Where SMSF trustees breach superannuation law the ATO can apply any one or more of the following compliance actions:

- imposing administrative penalties;[1]

- issuing education directions;[2]

- issuing rectification directions;[3]

- obtaining unenforceable undertakings that certain actions be implemented including the winding up of the SMSF;[4]

- disqualifying a person from being a SMSF trustee or a director of a SMSF trustee;[5]

- seeking court orders to impose civil and criminal penalties;[6]

- freezing the SMSF’s assets;[7] or

- making the SMSF non-complying which effectively results in the assets and income of the SMSF be taxed at 45%, an extremely adverse result.[8]

The first three compliance actions listed above only apply to superannuation law breaches which occur on or from 1 July 2014. Prior to this time, the ATO found it difficult to properly discipline SMSF trustees on superannuation breaches since the available compliance actions were not easy to take since civil or criminal penalties required court orders and making a SMSF non-complying was such an adverse action that it was rarely pursued. The enactment of the administrative penalties regime, education directions and rectification directions were aimed at providing the ATO with more flexible disciplinary powers.

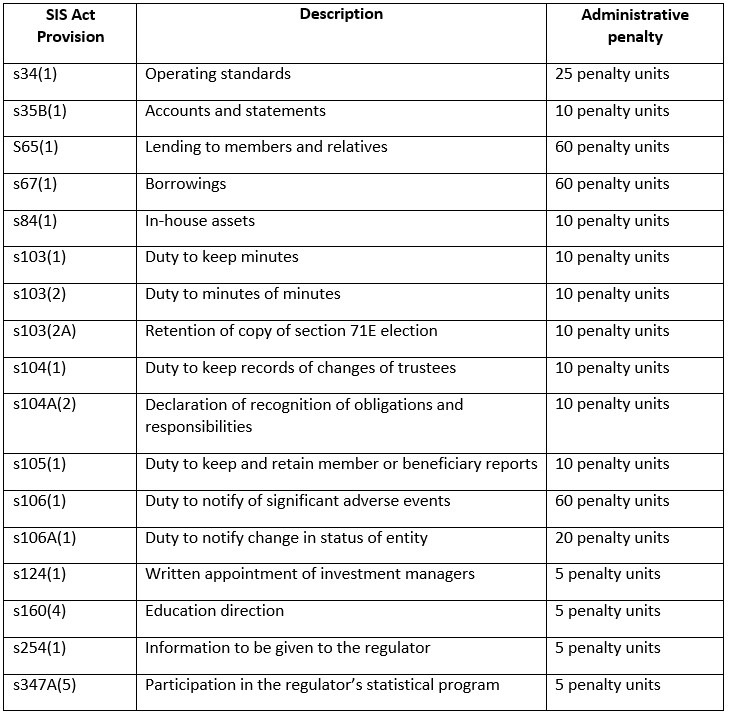

Under the administrative penalties regime, where a SMSF trustee breaches a superannuation provision listed in section 166 of the SIS Act, section 166 automatically imposes an administrative penalty. The following table lists the administrative penalty provisions and the amount of such penalty:

A penalty unit is CPI indexed every three years and currently is $222.

Not all breaches of superannuation law are listed in section 166 of the SIS Act. Significantly fault based breach provisions which rely on proof of fault based on criminal responsibility principles such as section 66 of the SIS Act (acquisition of an asset from a related party) are not listed. This is because breach of such provisions can lead to criminal penalties including imprisonment.

The way that the ATO conceives of a superannuation contravention in the Practice Statement is technical and can lead to multiple breaches (and hence multiple administrative penalties) where practically one might say that only one real breach has occurred. To the ATO’s mind there is no such thing as a continuing contravention which carries over successive financial years. Rather a contravention occurs at a particular point in time and if the breach remains unrectified at the end of the financial year, then a second contravention may be triggered.[9]

For instance, a SMSF may contravene the rule against lending to members under section 65(1)(a) of the SIS Act when it makes say a $10,000 loan to a member. If that loan is not repaid by the end of the financial year in line with the loan’s repayment schedule, then a second contravention occurs since the SMSF’s failure to seek repayment of the loan in accordance with the repayment schedule contravenes the rule against providing members with financial assistance in section 65(1)(b) of the SIS Act. That is, by failing to enforce the loan terms financial assistance has been provided. More breaches of this financial assistance rule will occur in each subsequent year where the SMSF trustee fails to repay the loan in accordance with its repayment schedule.

This technical approach to a contravention can result in significant administrative penalty amounts being imposed. For instance, if no repayments are made on the $10,000 loan to the member for three years this could lead to a prima facie $53,280 administrative penalty (i.e. $222 x 60 penalty units x 4). That is, five times the amount of the $10,000 loan! The approach taken in the Practice Statement is essentially to start from a high base of multiple penalties, and then focus on penalty remission.

The ATO’s stance on contraventions means loan breaches which have occurred prior to 1 July 2014 may still be dragged into the administrative penalty regime. For example, if a SMSF makes a loan to a member on 1 June 2014 the act of making of the loan is not subject to the administrative penalty regime. However, the SMSF’s failure to require repayment of the loan in accordance with the loan repayment schedule at the end of each subsequent financial year would constitute a breach on which an administrative penalty can be imposed.

The ATO’s position on contraventions reflects the statutory structure of the compliance test for a SMSF in section 42A of the SIS Act. Section 42A generally requires that a SMSF not contravene a regulatory provision on an income year by income year basis in order to continue to be a complying superannuation fund. Where a SMSF breaches a regulatory provision it only continues to be a complying superannuation fund at the discretion of the ATO.

Administrative penalties can be imposed on an individual SMSF trustee or a corporate SMSF trustee. It is important to note that where a SMSF has multiple individual trustees then it exposes the SMSF to multiple penalties for the one superannuation law breach. For example, where a SMSF has four individual trustees then a single breach of an administrative penalty may trigger 4 lots of the administrative penalty – one penalty for each individual trustee. Continuing on with our $10,000 loan example the total prima facie administrative penalty amount that can be imposed where the SMSF had four individual trustees is an eye watering $213,120 (i.e. 4 x $53,280).

Only one administrative penalty is imposed on a corporate trustee of a SMSF, however, its directors are jointly and severally liable to pay the penalty.[10] The fact that a corporate trustee is only subject to one administrative penalty for a breach whilst multiple penalties can apply where a SMSF has multiple individual trustees, is a significant reason besides ease of succession planning for a SMSF to have a corporate trustee rather than the individual members being trustees.

An administrative penalty can be also imposed on individual director of a corporate SMSF trustee for a failure to keep minutes,[11] failing to sign a trustee declaration form (declaring their recognition of the duties and obligations of a SMSF trustee) within the required time period[12] or failing to meet an education direction.[13]

Significantly a trustee cannot seek reimbursement from the SMSF for payment of an administrative penalty.[14]

How the ATO approaches penalty remission

The ATO has the power to remit the whole or part of an administrative penalty. A remission decision needs to be made for each trustee on whom the penalty is imposed, taking into account the trustee’s particular circumstances.

The fact that a trustee may not have been actively involved in a breach does not automatically lead to penalty remission. Example 9 of the Practice Statement describes a SMSF where the husband is the sole member but the trustees are the husband and wife. The husband makes all the decisions for the SMSF and various superannuation law breaches occur. The ATO did not consider that a further remission of administrative penalty was warranted for the wife. This was because ‘passivity’ is not an excuse since trustees are equally responsible to ensure appropriate controls are in place to prevent contraventions and each trustee needs to ensure they are fully informed about the actions of the other trustee.

The Practice Statement indicates that the ATO considers the following factors to be relevant in considering penalty remission:

- the purpose of the administrative penalty provisions which is to:

- encourage greater levels of voluntary compliance by ensuring there are consequences for non-compliance appropriate to the conduct;

- consistent treatment by specifying the penalty amount for each contravention; and

- shift trustee behavior so they do not contravene again;

- trustee behavior and individual circumstances:

- has the trustee generally tried to act with the care, diligence and skill that an ordinary prudent person would have exercised;

- what is the background, experience and intentions of the trustee;

- compliance history;

- has rectification occurred before ATO contact;

- was a voluntary disclosure made before ATO contact;

- were there circumstances outside the trustee’s control that caused the contravention, or affected a trustee’s ability to comply or rectify;

- the seriousness of the contravention – i.e. to what extent are SMSF assets affected and over what time period did the contraventions occur;

- does the prescribed penalty amount lead to an unintended or unjust result (e.g. is a cumulative penalty so large that it is excessive in light of the above factors);

- where multiple administrative penalties apply, is the cumulative penalty amount defensible, proper and just in light of the circumstances;For instance, if the multiple penalties arose from a single course of conduct or a particular event then remission may be warranted. In Example 10 of the Practice Statement a SMSF lends funds to a member and the member fails to repay the loan in accordance with the loan repayment schedule over a number of years. In such a situation the ATO imposed one administrative penalty for a breach of section 65(1)(a) of the SIS Act (the lending) and one administrative penalty for a breach of section 65(1)(b) of the SIS Act (failure to require repayment). The ATO remitted the administrative penalties imposed in subsequent years for failure to require repayment since they arose out of a single course of conduct in failing to require repayment.

- where multiple superannuation law provisions are breached, then the ATO will generally consider what is the primary contravention and remit the administrative penalty arising from secondary contravention. This is on the basis that the imposition of multiple penalties for one particular event is unjust. The primary contravention is determined based on the behavior and intention of the trustees.

For example, a SMSF loan to a member breaches section 65(1) of the SIS Act (loan rule) and also potentially section 84(1) of the SIS Act (in-house asset rules). In such a case the ATO considers the primary contravention is the breach of the loan rule.

Where a member access their superannuation benefits without meeting a condition of release then there is a breach of section 34(1) of the SIS Act (operating standards) and section 65(1)(b) (provision of financial assistance). In this situation the ATO considers the primary contravention is the breach of the operating standards.

Significantly, the Practice Statement indicates remission here depends on the circumstances of the case and remission should generally not be granted because of multiple penalties arising from one event in cases of fraud, evasion or egregious contraventions.

The penalty remission factors outlined in the Practice Statement are not exhaustive. The ATO describes its discretion to remit a penalty under section 298-20 of Schedule to the TAA in the Practice Statement as ‘unfettered’. This means that the ATO may remit the penalty in whole or part in any manner it wishes. However, this does not mean that the ATO can do anything it wants. Case law from tax cases indicates that the discretion should be exercised in light of the purpose behind the penalty provisions.[15] Additionally the case law indicates that the relevant question is whether it is appropriate in an individual’s circumstances to remit.[16] It is not necessary to show special circumstances for remission and remission may be appropriate where the outcome would be harsh in an individual’s particular circumstances.[17] Although it is not necessary to show harshness for remission to occur.[18]

A penalty remission decision must be provided in writing with and explanation. A SMSF trustee who is dissatisfied with a penalty remission decision may object and dispute it under Part IVC of the TAA.[19]

What should a SMSF trustee do now if there is a concern that there has been a superannuation law breach?

If you are a SMSF trustee or a director of a SMSF corporate and are concerned that your SMSF may have breached superannuation law, you should seek specialist superannuation law advice now. Depending on the circumstances it may be that the specialist advice may confirm that there is no breach of superannuation law at all. If there is a breach then strategies can be considered on how best to minimize penalties and regularize the situation. Such strategies may include implementing a rectification plan prior to or in conjunction with making a prompt voluntary disclosure to the ATO. Such a voluntary disclosure should comprehensively outline all relevant facts surrounding the breach including any rectification plan, and also the grounds for penalty remission. The key is rectifying and disclosing prior to the ATO initiating any compliance action.

The ATO has temporarily paused its superannuation compliance activities during this COVID time in light the financial issues faced by SMSF members. Instead the ATO encourages SMSF trustees to engage with them through its early engagement and voluntary disclosure service where breaches have occurred. Affected SMSF trustees should take advantage of this current ATO approach since the Practice Statement clearly indicates that penalty remission is a harder prospect in audit.

It is important to note that a key requirement of using the ATO’s early engagement and voluntary disclosure service that the SMSF be up to date in the lodgment of its annual returns. Accordingly, voluntary disclosure is usually a joint co-ordinated arrangement alongside the SMSF’s accountant.

Separately, SMSF members should seriously consider whether they should have a corporate trustee for their SMSF to minimise the administrative penalties which may be levied where a breach has occured. Whilst using a company involves annual ASIC fees (such fees can be reduced if the company’s sole purpose is to act as a SMSF trustee).

[1] Section 166 of the Superannuation Industry (Supervision) Act 1993 (SIS Act).

[2] Section 160 of the SIS Act.

[3] Section 159 of the SIS Act.

[4] Section 262A of the SIS Act.

[5] Section 126A of the SIS Act.

[6] Part 21 of the SIS Act.

[7] Section 264 of the SIS Act.

[8] Section 40(1) of the SIS Act and Subdivision 295 of the ITAA 97.

[9] Page 1 of PS LA 2020/3.

[10] Section 169 of the SIS Act.

[11] Section 103(2)(a) of the SIS Act.

[12] Section 104A(2) of the SIS Act.

[13] Section 160(4) of the SIS Act.

[14] Section 168 of the SIS Act.

[15] Paragraph 193 of Sanctuary Lakes Pty Ltd v FCT 2013 ATC 20-395.

[16] Sanctuary Lakes Pty Ltd v FCT 2013 ATC 20-395.

[17] Dixon as Trustee for the Dixon Holdsworth Superannuation Fund v FCT 2008 ATC 20-015.

[18] Sanctuary Lakes Pty Ltd v FCT 2013 ATC 20-395.

[19] Section 298-20(3) of Schedule 1 to the TAA.

Dung Lam provides clients with tax legal services and solutions. She has experience in advising on a wide variety of taxes including income tax, capital gains tax, GST and state taxes such as duty, payroll tax and land tax. Dung also has extensive experience advising on taxation trusts, superannuation issues in the self-managed superannuation funds arena and tax issues related to estate planning.

She works with clients and their advisers to devise tax effective strategies to undertake acquisitions and disposals of assets and businesses, business restructures, domestic and international business expansions, and succession planning. Dung also acts for clients in negotiations and disputes with Australian revenue authorities. She has managed ruling applications, tax risk reviews, tax audits, tax objections, voluntary disclosures, tax litigation and tax debt negotiations.

Clients whom Dung has assisted include corporates, high-net wealth individuals and families, and their advisers.

Dung is a Chartered Tax Adviser, Accredited Specialist in Personal and Business Tax with the NSW Law Society, a full member of the Society of Trusts and Estates Practitioners, member of the Law Council Revenue Law section and a member of the NSW Law Society’s Liaison Committee with Revenue NSW.

Prior to joining Coleman Greig Lawyers, Dung was a Senior Associate at both a national law firm and also a top tier international law firm.