Raymond Giblett, Partner and Timothy Chan, Associate at Norton Rose Fulbright Australia, question whether insurtech startups need to change up their compliance obligations. In this article, they reimagine the Product Disclosure Statement, the ‘promoting’ mindset and the sales channel.

Raymond Giblett, Partner and Timothy Chan, Associate at Norton Rose Fulbright Australia, question whether insurtech startups need to change up their compliance obligations. In this article, they reimagine the Product Disclosure Statement, the ‘promoting’ mindset and the sales channel.

Insurtech startups offering new products to consumers often face an interesting conundrum. After months of research, capital raisings, tech development and pitches, the startup finally reaches the pre-launch phase. At this point, the startup’s capacity partner (ie. insurer) suddenly decides to works with the insurtech on its ‘compliance framework’. More often than not, months of work including the vision of the customer journey is put aside while the insurer and startup rush to make the website, agreements and policy wording ‘compliant’. All involved do this in good faith, wanting to do the right thing before going live.

However, recent research and government royal commissions have shown that despite current compliance requirements, consumers still find it difficult to choose the most suitable insurance policy for their circumstances.[1] Is adoption of an insurer’s existing compliance framework at the eleventh hour, while ticking the legal boxes, the best way to disrupt a centuries old industry?

Back to the drawing board

There are a myriad of ways insurtech startups can redesign the customer experience while maintaining compliance with laws and regulations. In this article, we will explore two frequently overlooked areas with the potential to quickly improve the customer proposition and distinguish the insurtech from others in the market. Both areas require the cooperation of the insurer partner and the insurtech, so it is critical to work with a partner with an appetite to innovate.

Reimagining the PDS

In Australia, a large part of the compliance blitz involves the preparation of the Product Disclosure Statement (PDS). This is the document which sets out the details of the issuer, benefits of the product and details of the dispute resolution scheme. The policy wording is often included in the PDS.

The PDS disclosure regime was originally recommended by the Wallis Inquiry in 1997.The format of product disclosure statements has not been significantly challenged over the past two decades even though there is already flexibility in the current law to do so.

It is common for the startup’s insurer partner to insist on customising an existing PDS, mainly due to the time and cost savings associated with this option. Some insurers’ PDS documents are over 100 pages.

How can insurtechs get creative with the PDS?

A PDS must comply with specific content requirements prescribed by sections 1013C and 1013D of the Corporations Act 2001 (Cth), as well as disclosure requirements under the Insurance Contracts Act 1984 (Cth). However, there is considerable flexibility as to how the information may be presented as long as it is ‘clear, concise and effective’. A well designed PDS promotes customer understanding of the product as they can discover the benefits and exclusions more easily.

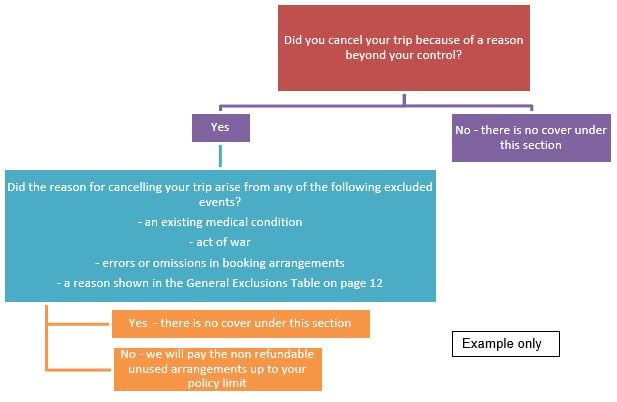

For example, a policy benefit can potentially be presented as a decision tree rather than a series of paragraphs. The below is an example of how a cancellation benefit within a travel insurance policy may be graphically depicted.

A decision tree is just one example. Within a PDS, a number of tools can be used in conjunction with each other to get a message across to the customer. A graphical depiction of a policy benefit could be accompanied by text or a link to a website where the customer can explore policy benefits in an interactive manner.

Time and effort is required to reimagine the PDS to make it truly customer centric, and the hardest part may be convincing key stakeholders who are accustomed to the traditional disclosure document. However, properly done, the rewards could be significant. A more readily understood PDS can potentially lead to fewer customer complaints, fewer disputed claims decisions and more satisfied customers who know what they are signing up for.

Moving from a ‘maintaining’ mindset to a ‘promoting’ mindset

Another area insurtech startups should examine is the sales channel. How can an insurtech assist the customer to disclose the necessary information the insurer needs to underwrite the product? The answer to this question requires a fundamental shift in the way the insurtech and insurer partner view compliance. The insurtech and insurer need to stop thinking about maintaining compliance and embrace promoting compliance.

Under section 21 of the Insurance Contracts Act 1984 (Cth), insurers (or their agent) are required to inform customers about their duty of disclosure. The customer’s duty of disclosure is an important obligation because it forms the basis of the insurer’s offer of insurance, including pricing, special excesses and any special conditions.

Questioning (in) the sales channel

Insurance sales websites differ in the way they inform customers about their duty of disclosure. Sometimes it is a pop up message, expandable text message, squeezed in to the side, or inserted just before the underwriting questions. However, while these may potentially enable the insurer to discharge its obligation to inform the customer of their duty, it still leaves the customer in the lurch to answer the questions. This could result in a poor customer experience and inaccurate information collected, especially if the questions involve jargon, are difficult to understand, or appear to be an endless list. The negative experience is potentially compounded if the customer makes a claim and the insurer uses the customer’s answers against them to deny or reduce a payout.

Insurtechs designing a new insurance product might like to consider how the disclosure process can be simplified through the use of existing and accurate data, so the customer answers fewer questions. For example, satellite images and local council data can be used to pre-populate key property attributes relevant to the underwriting decision. In home insurance, this could include the type of roof, size of the property, existence of a pool and proximity to trees.

It also remains to be seen whether the insurance sector may be subject to Australia’s Consumer Data Right (CDR) in the future. The CDR allows customers to access and transfer data about them by businesses to third parties of their choice. The CDR is currently being implemented in the banking sector and will then roll out in the energy sector. The CDR is intended to help consumers compare products in the sectors where it operates.

Another reason to give these ideas more thought is because the duty of disclosure is proposed to become a duty to take reasonable care not to make a misrepresentation. The scope of the insured’s duty is narrower under the proposed test so it is in the insurer’s interest to be able to capture accurate information from a reliable source while simultaneously improving the customer’s experience in the sales channel.

Tips and tricks

These are just some ways for insurtech startups and their insurer partners to get creative with compliance. As startups create the insurance products of the future, and consumers demand more tailored products, compliance should also evolve. While there is room to reimagine compliance within the current legislative framework, there is certainly even more room to rethink the framework altogether. The Australian Law Reform Commission has commenced a review of the financial services regulation framework. The review will run from 2020 to 2023.

In the meantime, rather than leaving compliance to the last minute, startups can reap the rewards if they are proactive and rethink how they can tick the box while providing a unique and better customer experience.

[1] Australian Securities and Investments Commission and Dutch Authority for Financial Markets, ‘Report 632: Disclosure – Why it shouldn’t be the default’ (October 2019) <https://download.asic.gov.au/media/5303322/rep632-published-14-october-2019.pdf>; Commonwealth, Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Final Report (2019) vol 1.

Ray Giblett is a partner in our Sydney office and an insurance lawyer with over 20 years’ experience. Ray is recognised as one of Australia’s leading insurance lawyers in Chambers Asia Pacific, Legal 500, Best Lawyers (2013 Sydney Insurance Lawyer of the Year) and Euromoney’s guide to the World’s Leading Insurance and Reinsurance Lawyers. Connect with Ray via email or LinkedIn![]()

Timothy Chan is an insurance lawyer based in Sydney. Providing advice on the full spectrum of insurance matters, Tim regularly works with clients on the set up of insurance businesses, distribution issues, licensing in Australia, reinsurance and coverage disputes. He also has experience advising financial institutions on eligible regulatory capital requirements under APRA’s prudential standards, and the use of specialist risk transfer solutions. Connect with Timothy via email or LinkedIn![]()