Kelly+Partners Tax Legal’s Senior Client Director Tony Nunes, CTA, and Senior Tax Consultant Jane Harris, FTI, discuss changes to the Small Business CGT Concessions (SBCGT). The changes apply to taxpayers using the SBCGT concessions for the sale of shares in a company or units in a trust, they write. Tony and Jane recently gave a presentation on this topic for Legalwise Seminars.

Kelly+Partners Tax Legal’s Senior Client Director Tony Nunes, CTA, and Senior Tax Consultant Jane Harris, FTI, discuss changes to the Small Business CGT Concessions (SBCGT). The changes apply to taxpayers using the SBCGT concessions for the sale of shares in a company or units in a trust, they write. Tony and Jane recently gave a presentation on this topic for Legalwise Seminars.

Taxpayers that have sold CGT interests in a company or trust after 8 February 2018 are affected by the changes and need to ensure that they have applied the new rules.

Modified active asset change

There are a number of changes to the SBCGT concessions. However, one of the key changes is the introduction of a modified active asset test, which broadly looks through to the underlying assets of the entities in which the interests are held.

The changes make it harder to meet the active asset test – under the modified active asset test, a proportion of all the assets of entities in which the taxpayer owns an indirect interest (“a later entity”) are counted in the pool of assets. However, these assets can only count as “active” if:

- the taxpayer’s small business participation percentage in the later entity is greater than 20% or the taxpayer is a CGT concession stakeholder of the later entity.

- The later entity would be a CGT small business entity or satisfy the MNAVT (using the 20% control test rule).

Lowering of the “control percentage”

Relationships with larger businesses, that in past would not necessarily prevent access to the SBCGT concessions, will likely do so now as for the purposes of determining whether the additional basic conditions are met, the ‘control’ percentage has been lowered from 40% to 20%.

The object entity must be a CGT small business entity (i.e. have an aggregated turnover of less than $2 million) or satisfy the modified Maximum Net Asset Value (“MNAV”) test,[1] where an entity is connected with another entity if it satisfies the 20% control test[2]. Thus where an entity is connected with any entity (using the 20% control test) that is not a small business entity, the first entity will also fail the small business entity requirement.

Below are some examples of how the new rules apply

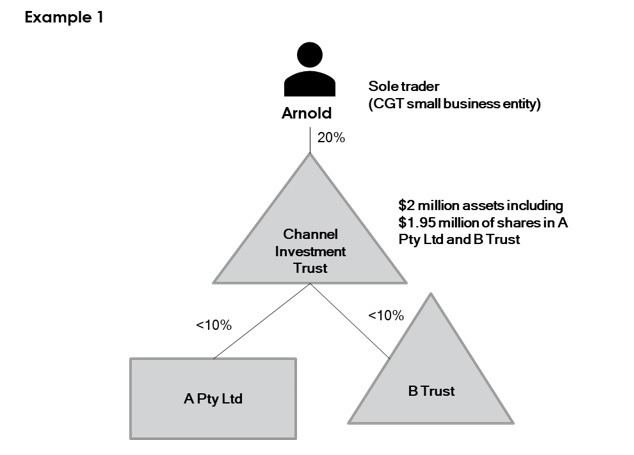

In example 1, Arnold sells his 20% interest in Channel Investment Trust. [3] While Arnold may satisfy the basic conditions for relief for the capital gain, he does not satisfy the new conditions. The investment in Channel Investments Trust does not satisfy the modified active asset test as 97.5% of its assets are shares and interests in trusts that are considered passive assets as its small business participation percentage in the relevant entities is less than 20%.

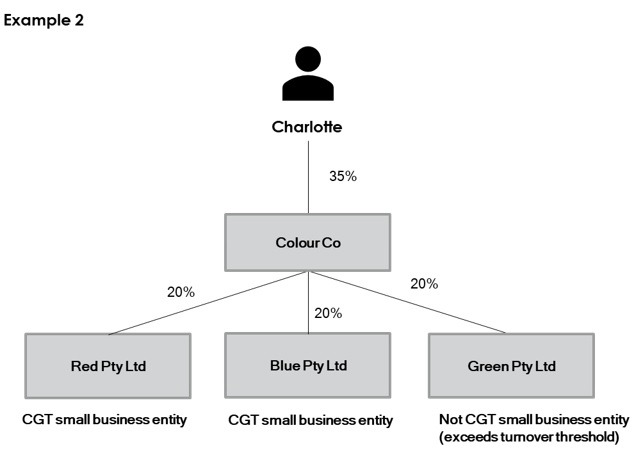

In example 2, Charlotte sells her shares in Colour Co.[4]

In working out if this interest satisfies the modified active asset test, the total value of the assets of Colour Co does not include the value of the shares it holds in Red Co, Blue Co and Green Co; however, it includes 20% of the value of the assets of these companies.

Further, for the purposes of the modified active asset test, assets of later entities are only “active assets” if the entity is a CGT small business entity or satisfies the maximum net asset value test. Green Co is not a CGT small business entity as its turnover is too high.

Additionally, Charlotte must treat Red Co, Blue Co and Green Co as being connected with Colour Co and with each other for the purposes of the test, because Colour Co holds 20% of the shares of each entity. Because they are treated as being connected with Green Co, Red Co and Blue Co are also not CGT small business entities for these purposes. As a result, Charlotte is not able to treat the assets of Red Co, Blue Co or Green Co as active assets for the purposes of this test unless the entities satisfy the maximum net asset value test.

The modified active asset test makes it more difficult for a taxpayer to satisfy the active asset test, given that less assets can be included as active assets of an entity.

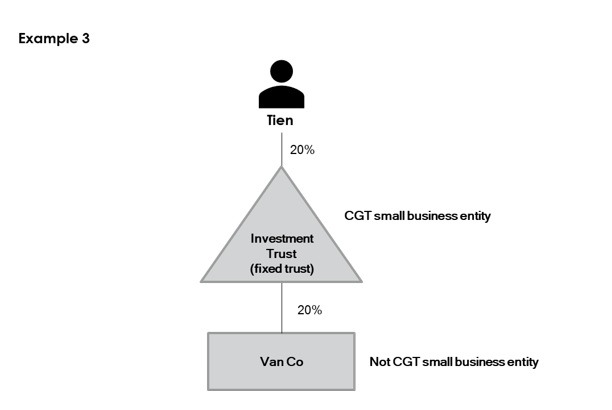

In example 3, Tien sells his 20% interest in Investment Trust (a fixed trust).[5] Investment Trust satisfies the small business entity test, but Van Co does not. Van Co’s net asset value exceeds $6 million.

Investment Trust is connected with Van Co given that it holds 20% interest in Van Co (a controlling percentage for the purposes of the additional basic conditions). Accordingly, Investment Trust does not satisfy the CGT small business entity definition nor MNAVT when it includes the turnover and the assets of Van Co.

Planning is key

The above examples highlight some of the key changes and how they apply. Taxpayers should carefully review their existing group structure and any indirect interests an entity has in other entities in light of the new thresholds for ‘connected’ entities. Advice should be sought on whether a restructure is possible where a taxpayer has lost access to the SBCGT concessions due to the new amendments.

Tony Nunes, CTA (Senior Client Director) is a taxation specialist for families and businesses and has extensive experience in business structuring, business sales and acquisitions, cross-border taxation issues, employee incentive and compensation programs and in dealing with ATO and state audits. Tony is an admitted Solicitor of the Supreme Court of NSW and holds Bachelor of Commerce, Bachelor of Law and Master of Law and Master of Taxation degrees. Contact Tony at Tony.nunes@kellypartners.com.au

Jane Harris, FTI (Senior Tax Consultant) has over 10 years of experience assisting high net wealth and SME clients with taxation matters. At Kelly+Partners, Jane provides clients with structuring, negotiation and tax legal advice, predominantly in income tax. Jane is an admitted Solicitor of the Supreme Court of NSW and holds Bachelor of Commerce, Bachelor of Arts and Juris Doctor degrees from the University of Sydney. Contact Jane at Jane.harris@kellypartners.com.au

You can also connect with Kelly+Partners via LinkedIn, Facebook or Twitter

[1] s 152-10(2)(c).

[2] s 328-125.

[3] Explanatory Memorandum Treasury Laws Amendment (Tax Integrity and Other Measures) Bill 2018 example 2.3.

[4] Explanatory Memorandum Treasury Laws Amendment (Tax Integrity and Other Measures) Bill 2018 example 2.2.

[5] Explanatory Memorandum Treasury Laws Amendment (Tax Integrity and Other Measures) Bill 2018 example 2.5, modified to show outcome for fixed trust.